By ATGL

Updated January 31, 2025

[ez-toc]

In the world of investing, risk is unavoidable — but it can be measured, managed, and mitigated. One of the most widely used tools for assessing financial risk is Value at Risk (VaR). This metric helps investors, financial institutions, and risk managers quantify potential losses within a given timeframe and confidence level. But how exactly does VaR work, and what are its limitations? In this guide, you’ll learn about the concept of VaR, explore its calculation methods, and see how it fits into a broader risk management strategy.

What Is Value at Risk (VaR)?

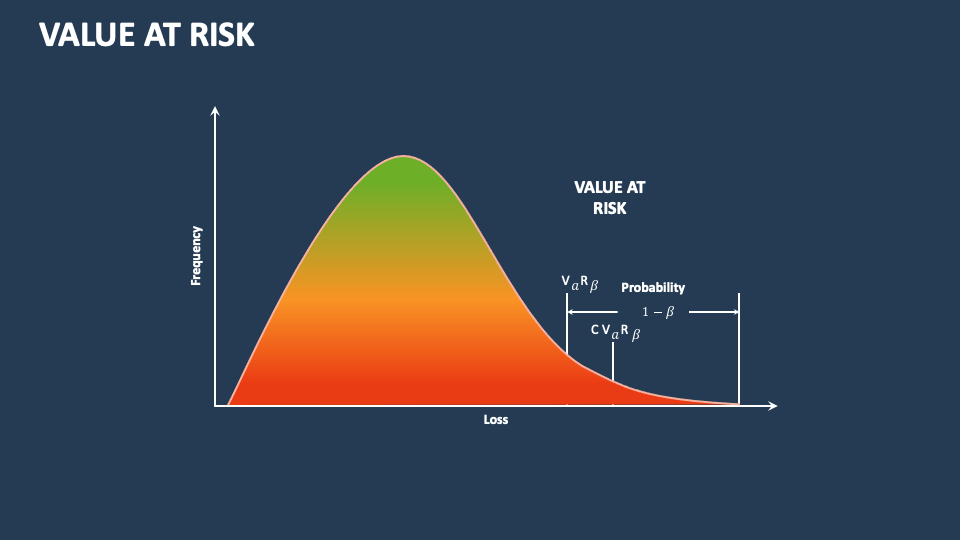

Value at Risk (VaR) is a widely used risk management metric that quantifies the potential loss in an investment or portfolio over a given time frame at a specific confidence level. Financial institutions, asset managers, and investors use VaR to assess market risk exposure and make informed decisions about risk mitigation strategies.

In simple terms, VaR answers the question: What is the worst expected loss under normal market conditions within a given time period at a given probability?

Why Is VaR Used in Financial Risk Management?

VaR is important in financial risk management because it provides a standardized way to measure risk across different asset classes and portfolios. Its primary benefits include:

- Simplicity: VaR condenses risk into a single number, making it easy to interpret.

- Comparability: It allows investors and institutions to compare risks across different portfolios.

- Regulatory Compliance: Many financial regulators, such as Basel Accords for banks, require VaR reporting for capital adequacy assessment.

However, VaR is not without its limitations, as it assumes normal market conditions and may not capture extreme events such as financial crashes.

Understanding Conditional Value at Risk (CVaR)

Conditional Value at Risk, also known as Expected Shortfall (ES), is an extension of VaR that provides a more comprehensive risk measure. Unlike VaR, which only looks at the threshold of potential loss, CVaR considers the average loss beyond the VaR threshold.

Why Is CVaR Important?

- It accounts for tail risk, which is the likelihood of rare but severe market events that fall outside the normal distribution of returns. This is critical for understanding extreme market movements.

- CVaR provides a more conservative estimate of risk, making it useful for risk-averse investors.

- It is increasingly being used in risk-adjusted portfolio optimization.

While VaR provides a cutoff point, CVaR goes deeper, giving investors a clearer picture of worst-case scenarios.

VaR Calculation: Top 3 Methods Explained

There are three primary methods for calculating VaR:

1. Historical Simulation

This method uses historical data to determine potential losses. It involves:

- Collecting past returns of the portfolio over a given time frame.

- Sorting the returns from worst to best.

- Identifying the loss at the desired confidence level (e.g., 95%).

Pros: There’s no need for complex modeling, and it captures actual past market behavior.

Cons: It assumes that past market trends will continue, which may not always hold true.

2. Monte Carlo Simulation

This approach generates thousands (or millions) of hypothetical market scenarios based on statistical models and computes potential losses. It involves:

- Simulating random price movements based on probability distributions.

- Running thousands of trials to estimate the worst-case loss at a given confidence level.

Pros: It’s highly flexible and can incorporate different market conditions.

Cons: It’s computationally intensive, and accuracy depends on model assumptions.

3. Variance-Covariance Method (Parametric VaR)

This method assumes that asset returns follow a normal distribution and calculates VaR using statistical formulas. The formula is:

VaR = Zα X σ X √t

where:

- Zα is the z-score corresponding to the confidence level (e.g., 1.65 for 95%).

- σ is the portfolio standard deviation.

- t is the time horizon.

Pros: It’s fast, efficient, and widely used in financial models.

Cons: It assumes normal distribution, which may underestimate extreme losses.

Key Benefits and Limitations of VaR

VaR is a valuable risk management tool, but knowing where it excels and where it falls short is key to applying it effectively.

Advantages of Using Value at Risk

- Easy to interpret: A single number provides a clear risk metric.

- Regulatory recognition: Used by banks and financial institutions to report risk.

- Applicable across assets: Can be used for stocks, bonds, derivatives, and portfolios.

Downsides and Limitations of VaR

- Fails to capture extreme risks: Doesn’t consider black swan events.

- Different methods yield different results: VaR depends on the chosen calculation method.

- Assumes normal market conditions: Market crashes often violate these assumptions.

Despite these limitations, VaR remains a core risk management tool, especially when supplemented with other metrics like CVaR and stress testing.

Key Aspects of Value at Risk Modeling

VaR is a powerful risk management tool, but to get the most out of it, you need to set the right parameters, choose the best calculation method, and know how to interpret the results. Here’s how to make VaR work for you.

Setting Parameters: Confidence Levels, Time Horizons, and Loss Measurement

- Confidence Levels: Typically set at 95% or 99%, meaning there’s a 5% or 1% chance of exceeding the estimated loss.

- Time Horizons: Can be daily, weekly, or annual, depending on how often you assess risk.

- Loss Measurement: Expressed as absolute VaR (a dollar amount) or relative VaR (a percentage of the portfolio).

VaR is often used alongside other risk measures, such as systematic risk and unsystematic risk, to better understand both market-wide and asset-specific volatility.

Choosing the Right Calculation Method

Different methods offer different insights:

- Historical Simulation: Simple and based on past data, but not optimal for predicting extreme market events.

- Monte Carlo Simulation: Runs thousands of possible market scenarios, making it flexible but computationally intensive.

- Variance-Covariance Method: Quick and efficient but assumes normal market conditions, which isn’t always realistic.

For a clearer picture, many investors use a mix of these methods. If you’re using the Capital Asset Pricing Model, VaR can be a complementary tool to measure how risk-adjusted returns align with expected market performance.

Interpreting VaR in Risk Management

VaR is a useful benchmark for assessing potential losses, but it has its limitations:

- What It Tells You: The maximum expected loss within a given time frame at a specific confidence level, assuming normal market conditions.

- What It Doesn’t Tell You: The likelihood or impact of extreme market events (e.g., financial crashes or black swan events), the sources of risk, or how losses might compound in times of market stress.

To get a full view of risk exposure, VaR should be paired with:

- CVaR: Looks beyond the worst-case threshold for deeper insights.

- Stress Testing and Scenario Analysis: Models extreme situations to prepare for the unexpected.

By integrating VaR with other risk strategies, you can build resilient portfolios. For example, if you’re focused on long-term portfolio stability, you can integrate VaR with a dividend growth strategy, using risk metrics to balance income generation with downside protection.

Ensure Profitable Financial Investments With Above the Green Line

Understanding and applying VaR can help you navigate market volatility and make better-informed investment decisions. However, managing risk effectively requires more than just calculations — it requires strategic insight and professional guidance.

At Above the Green Line, we offer expert investment strategies that help you grow your portfolio while managing risk efficiently. Join us today and start making smarter investment decisions.

Related Articles

[pt_view id=”b47aec5l7b”]